New office space requirements increased by 29 percent in Q2 2021 compared to Q1 across Africa according to Knight Frank.

This increased office market activity has been attributed to the ‘flight to quality’ trend that has seen businesses taking advantage of weakened prime office rents to occupy office spaces that place employee wellbeing at the forefront as well as improving economic outlook across most of the countries.

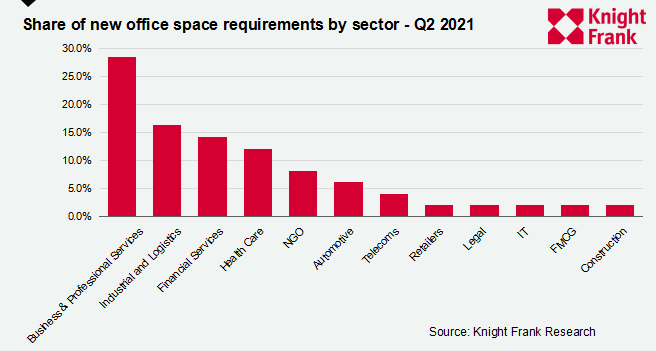

Data from Knight Frank indicates that the share of new office space requirements across the nine countries they are located in (Kenya, Uganda, Nigeria, Tanzania, Zambia, Zimbabwe, Malawi, Botswana, South Africa) was dominated by Professional Services (29 percent), Industrial & Logistics (16 percent), Financial Services (14 percent), Healthcare 12 percent and NGOs (8 percent), who together accounted for almost 80 percent of new office space requirements across Africa in Q2, indicating a return in business confidence in these sectors.

Knight Frank also observed that businesses that had previously put office requirements on hold due to the pandemic were reactivating their searches with landlords becoming more flexible by allowing for discounted rents and lease concessions such as increased rent-free periods in a bid to attract and retain tenants.

Knight Frank also observed that businesses that had previously put office requirements on hold due to the pandemic were reactivating their searches with landlords becoming more flexible by allowing for discounted rents and lease concessions such as increased rent-free periods in a bid to attract and retain tenants.

“The overarching trend across Africa’s office market is the continued flight to quality. Occupiers remain focussed on occupying best-in-class offices that offer greater flexibility around lease terms. The desire to occupy the best office buildings is driving up tenant release space in some cities’ Grade B buildings, which is likely to fuel greater disparity between the performance of Grade A and Grade B office rents. That said, this presents a real opportunity for landlords of slightly older buildings. If refurbished to a new, modern standard, they can compete effectively for tenants looking for high-quality offices,” says Tilda Mwai, Senior Researcher Knight Frank Africa.

Across the 28 African cities Knight Frank monitors, prime headline office rents remained relatively resilient with 16 out of the 28 cities tracked experiencing rental stability during the review period. However, market performance continues to vary based on the country.

In Nairobi for example, prime office rents dropped marginally by one percent q-o-q due to lockdown restrictions imposed at the onset of Q2 2021. In addition, markets such as Western Cape and Gauteng in South Africa continue to see increased vacancy rates and downward pressure on prime rents, prompting landlords to offer incentives and discounts.

Nigeria recorded increased occupier activity in the market driven by office relocations from the CBD to the suburbs, as occupiers gravitated to locations offering both better quality accommodation, as well as more affordable lease rates.

Occupier activity in locations such as Tanzania is expected to recover underpinned by renewed investor confidence fuelled by the new leadership.

Nairobi has continued to see a gradual return in business confidence reflected by the increased number of business entities registered. According to the Registrar of Companies there was a 25 percent month-on-month change with 8,483 companies registered in July 2021 compared to 6,786 companies registered in June 2021. Knight Frank anticipates this will result in increased demand for offices later in the year.

Read: >>> Huawei Kenya Launches IdeaHub Products for Smart Office and Education Needs

>>> Tenants in Control as Nairobi Offices Drop Rents Under Pressure

![Parliament in a past session. [Photo/Parliament of Kenya/Facebook]](https://businesstoday.co.ke/wp-content/uploads/2026/02/Parliament-Kenya-200x143.webp)

![[Photo/ Kanu|Twitter]](https://businesstoday.co.ke/wp-content/uploads/2022/11/bae8f7b06202ff2c-1.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment